How Does Section 754 Election Work

Go to Form Sch K-1 1065. In this case a partnership can recover basis it would otherwise lose if the 754 election were not in.

Consequences Of A Section 754 Election

754 election at any time does not require the occurrence of a triggering event.

How does section 754 election work. Select the Special Alloc tab. Situations Where a Basis Adjustment Can Be Made. This election allows the new partner to receive the benefits of depreciation or amortization that he or she may not have received if the.

A valid election requires strict adherence to procedural guidelines including the filing of a written statement with the partnerships tax return in the year that the distribution or sale occurred. This step-up in basis is used to make the outside basis basis of the partnership in the hands of the owner equal to the inside basis the basis of the assets in partnership for tax. How and Why to Make a 754 Election.

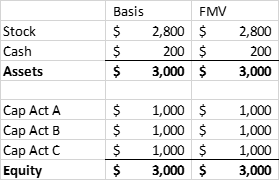

Distribution of partnership property or transfer of an interest by a partner. Section 754 elections are available only to partnerships and LLCs taxed as partnerships for which the entitys income and losses pass through to each partner. And Outside Basis Inside basis is the total equity the partnership has in its assets whereas Outside basis is each partners tax basis in their share of the ownership.

Making the Section 754 election is a big deal if your client is in the midst of handling partners partnerships and property distributions to partners. Making the Election. 1014 a 1.

Whether or not an election under section 754 is in effect the basis for each of the remaining partnership interests will be 39050 20000 original contribution plus 12000 each partners original share of the liabilities plus 6000 the share of Cs liabilities now assumed plus 1050 each partners share of ordinary income realized by the partnership upon that part of the distribution treated as a sale or. 754 to adjust the basis of partnership property under Secs. Under the Section 754 regulations however an application to revoke the election will not be approved if the revocations primary purpose is to avoid stepping down the basis of partnership assets.

The name and address of the partnership. An election made under the provisions of this section shall apply to all property distributions and transfers of partnership interests taking place in the partnership taxable year for which the election is made and in all subsequent partnership taxable years unless the election is revoked pursuant to paragraph c of this section. Under section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred.

Statement of Section 754 Election i. The purpose of a Section 754 election is to reconcile a new partners outside and inside basis in the partnership. Partnership may make the Sect.

Sec 754 Depreciation select 0 - By Amount or a Special Allocation number from the Special Allocation drop-down menu. November 13 2018. The purpose of the adjustment is to eliminate the difference between inside basis of the partnership property and the.

El ti i fil d ith ti l fil d t hi t i l di Election is filed with a timely filed partnership return including extensions. 1754-1b1 provides that an election under Sec. 743b provides that in the case of a sale or exchange of a partnership interest for which a Sec.

734b and 743b shall be made in a written statement filed with the partnership return for the tax year during which the distribution or transfer occurs. Election must be signed by a partner. Select the Yes check box on Line 12a - Is the partnership making or had it previously made and not revoked a section 754 election.

Under Section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred. The statement must include. A Section 754 election applies to all property distributions and transfers of partnership interests during the partnership tax year for which the election is made plus for all later tax years unless revoked.

Generally a person receiving a partnership interest upon the death of a partner receives that interest with a basis equal to the fair market value of the interest immediately before the partners death plus any assumed partnership liabilities. Contributions Distributions Basis. Select the Ln 13d Sch K - Oth Ded tab.

- The partnership has made a section 754 election that is effective in the year of the sale or exchange - The partnership has a substantial built-in loss immediately after the transfer Section 743d1 provides that a partnership has a substantial built-in loss. The Section 754 election can also apply when a partnership makes a distribution of property and the basis of the distributed property to the partnership and the basis the partnerdistributee will take in the distributed property are not equal. Section 754 provides that if a partnership files an election in accordance with regulations prescribed by the Secretary the basis of partnership property is adjusted in.

754 election is in place a partnership shall adjust the basis of partnership property. Section 704c-Introduction If basis of contributed property differs from its Section 704b II book value Section 704clA requires income gain loss and deduction with respect to such property to be allocated among the partners 11 SO as to take account of the variation between the basis of the property to the partnership and its FMV at. The purpose of a Section 754 election is to reconcile a new partners outside and inside basis in the partnership.

Two statements should be attached to the return for the taxable year during which the distribution or transfer occurs. At the formation of a partnership inside and outside basis are usually equal. The Section 754 election must be made before the due date of the income tax return including extensions for the year in which the transfer occurs.

Section 743c provides that the allocation of basis among partnership properties where 743b is applicable shall be made in accordance with the rules provided in 755. This is done by adjusting the partnerships basis in those assets inside basis to align with the partners basis in the partnership outside basis. The Section 754 election must be made in a statement that is filed with the partnerships timely filed return including any extension for the tax year during which the distribution or transfer occurs.

At a high level the purpose of the Section 754 election is to align inside and outside basis to avoid these scenarios. Section 754- Making the Election For a Section 754 Election to be valid a written statement must be attached to the partnership return and filed no later than the return due date including extensions. Under Line 13 - Code W Items.

Section 754 allows a partnership to make an election to step-up the basis of the assets within a partnership when one of two events occurs.

Avoid Costly Tax Issues By Considering The Section 754 Election Businesswest

V3 Bfj Jh38f3m

Weekly Steps Tracker Pedometer Step Tracker Steps Log For Pedometer Weekly Step Record Walk Planner Pedometer Tracker 12 Step Recovery Worksheets Graphing Linear Equations Activities 12 Step Worksheets

Letter To Bergdorf Goodman After Election Jackie Kennedy Jackie Kennedy Style Kennedy

Online Video Editor Free No Watermark For Youtube In 2021 Video Online Video Editor Writing Paper

Partnership Taxation What You Should Know About Section 754 Elections

Partnership Taxation What You Should Know About Section 754 Elections

How Non Profits Can Maximize Office Productivity With Managed It Managed It Services Cyber Security Network Monitor

Gxhsiehvb71r6m

Consequences Of A Section 754 Election

Section 754 Elections Theory Practice Youtube

Advantages Of An Optional Partnership Basis Adjustment

What Is Stumbleupon And How To Use It Social Media Stumbleupon New Twitter

An Alternate Route To An Ipo Up C Partnership Tax Considerations Part 2

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

Pin By Clint On Exposing Diabolical Leftist Sidney Powell Power To The People

Advantages Of An Optional Partnership Basis Adjustment

Partnership Taxation What You Should Know About Section 754 Elections

A Business Must Pay A Variety Of Taxes Based On The Company S Physical Location Ownership Structure And Nature Of The Business Log Business Tax Business Tax

{kind=link}

Post a Comment for "How Does Section 754 Election Work"